➡️Download this customizable article

A strategy that minimizes income taxes over a long retirement can help you stretch and keep more of your money.

Planning for retirement can be both exciting and, well, not so much. Envisioning where you want to live and the places you want to visit is a satisfying aspect of retirement planning. Contemplating taxes in retirement is not as thrilling.

Nevertheless, paying attention to taxes can have a significant impact on your ability to live the lifestyle you want in retirement. Having a strategy that minimizes your income taxes over the course of a long retirement can help you stretch your money— and keep more of it.

Balancing your need for both savings growth and reliable income is also a critical part of a retirement income plan.

Why taxes matter

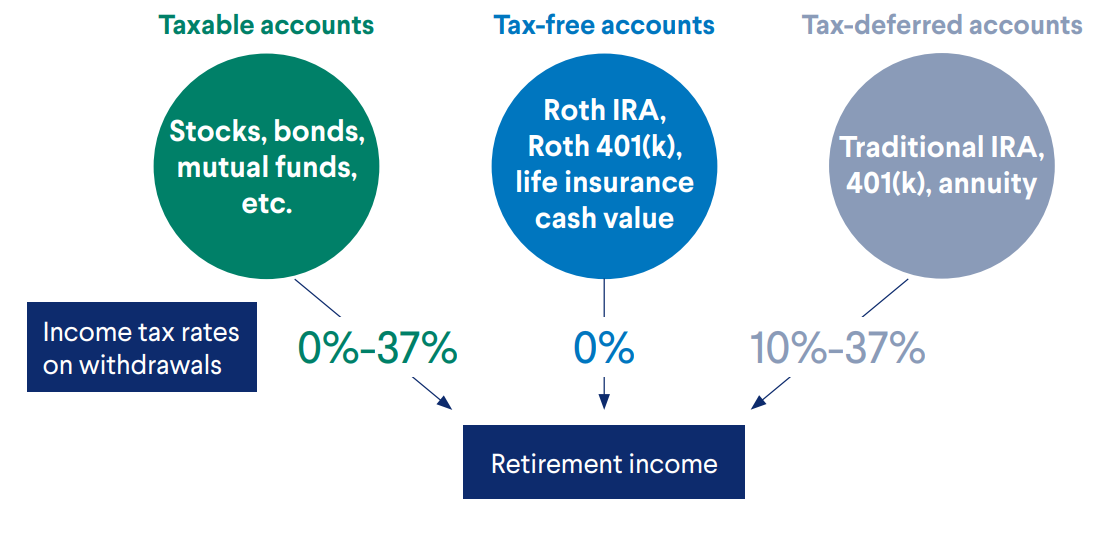

Like most people, you most likely have retirement savings in a variety of places—such as IRAs, 401(k) plans, annuities, and taxable investment accounts at a brokerage or bank. These accounts differ significantly in how withdrawals are taxed. Depending on the account you’re withdrawing from, it may be tax free or it may be taxed as ordinary income or capital gains.

Retirement tax strategies will vary based on the types of accounts you have, how your assets are distributed, and your income needs. Getting help from a financial professional is essential. When you’re ready to have this important strategy discussion, you’ll benefit from having some basic knowledge of the various ways that your savings are taxed and the considerations that go into deciding which accounts to access and when.

Types of income

While you were accumulating retirement assets during your working years, you were probably advised to diversify your investments. The idea was—and is—to spread your assets among various economic sectors and investment types that behave differently under different economic conditions.

When you’re ready to begin withdrawing your retirement assets, you’ll soon discover that the same principle applies to taxes. Having assets in a variety of accounts governed by different tax rules enables you to be strategic about how you set up your retirement income plan. Assuming you don’t incur penalties by withdrawing from your qualified retirement savings accounts too soon—before age 59½—here’s an overview of how the most common types of retirement accounts are taxed:

Traditional IRA and 401(k). The big benefit is tax deferral. You don’t pay income tax on your deductible contributions the year you make them or on investment earnings in the year they’re credited. This allows savings to grow faster during the deferral period. Taxes are due when you withdraw the money. You can postpone taking distributions until age 73 (age 75 if born in 1960 or later), but from then on you have to take annual required minimum distributions (RMDs) using an IRS formula based on your life expectancy. Distributions are taxed as ordinary income.

Roth IRA and Roth 401(k). Unlike qualified contributions to traditional retirement accounts, Roth account contributions were fully taxed when you made them. Generally, you won’t owe any tax when you begin withdrawing the money in retirement—either on what you contributed or any earnings. Plus, RMDs are not required for owners of Roth IRAs during life.

Brokerage and bank and investment accounts. Money invested in stocks, bonds, or mutual funds in a taxable account is taxed only on the amount of money you withdraw that represents a capital gain—the amount that the initial investment increased in value. Taxes on long-term capital gains—on investments held for at least one year—range from 0% to 20%, depending on your total taxable income. Short-term capital gains—on investments held less than one year— are taxed as ordinary income.

Deferred annuities. The tax owed on payments from a deferred annuity in retirement depends on how you purchased the annuity. If you used pretax money from a traditional IRA or 401(k), for example, the payments you receive from an annuity are fully taxable, and you are subject to RMDs once you reach age 73. If you purchased the annuity with after-tax money, you owe tax only on the amount of the withdrawal attributed to interest generated by the annuity. There are no mandatory withdrawals during life, unless they’re part of the annuity contract.

Tax treatment of distributions

Tax planning considerations

As you consider the tax implications of all of these potential income sources, the question is which one (or ones) you should access first. The answer depends on many factors, but conventional wisdom has long held that it’s preferable to withdraw from taxable accounts first, then move to traditional retirement accounts, and, finally, to Roth retirement accounts.

More-recent thinking indicates you could benefit by withdrawing from tax-deferred accounts first or tax-deferred and taxable accounts simultaneously, depending on your income needs and tax situation. Not only could the latter approach help you avoid major fluctuations in your taxes at different stages of your retirement, it could increase the longevity of your savings. Let’s compare a few different scenarios.

Scenario 1: Taxable accounts first

By withdrawing from your taxable accounts first, you may be able to avoid paying income tax on withdrawals in the beginning of your retirement and for as long as the money in those accounts lasts. This allows the money in your traditional IRA or 401(k) to potentially continue growing while tax payments are pushed further into the future.

Cashing out of brokerage accounts first might not generate capital gains taxes because the tax rate on longterm capital gains is zero for married couples filing jointly who have taxable income up to $96,700 in 2025. If their taxable income is between $96,701 and $600,050, the rate will be 15%, and for jointly filing couples with income above $600,051 the capital gains tax will be 20%. Tax rates on ordinary income, by comparison, range from 10% to 37% across seven marginal tax brackets.

Keep in mind, a 3.8% surtax on net investment income applies to married filing jointly taxpayers with a modified adjusted gross income of more than $250,000, due to the Affordable Care Act.

Scenario 2: Tax-deferred accounts first

Why would you want to withdraw money from a tax-deferred account and owe ordinary income tax instead of withdrawing money potentially tax free from a brokerage account? Because you might be better off paying taxes now rather than later: for instance, if your income needs allow you to take withdrawals that stay within the 12% tax bracket, which in 2025 applies to income between $23,851 and $96,950 for married filing jointly.1

If you wait to withdraw from your traditional IRA until you have to take RMDs, you could push yourself into a higher bracket (and pay higher taxes) later in retirement. Over the course of a long retirement, this strategy could increase the longevity of your retirement savings.

Scenario 3: Taxable and tax-deferred combined

This approach combines the advantages of the first two strategies. By drawing income from multiple sources, you may be able to stay within a low tax bracket while taking advantage of opportunities to convert tax-deferred savings into tax-free withdrawals later in retirement.

Get a personalized plan from a professional

These three strategies and examples offer a high-level view of smart tax management to potentially lower your taxes in retirement and extend the longevity of your savings. Tax law is complicated, however, and each individual’s situation is different, so developing a plan that works best for you requires professional help.

1Internal Revenue Service, Rev. Proc. 2024-40, https://www.irs.gov/pub/irs-drop/rp-24-40.pdf